Pre 59 ½ IRA Withdrawals Penalty Free -72(t) Strategy

If you’re under 59½ and need steady income from your IRA, a 72(t) SEPP (Substantially Equal Periodic Payments) lets you avoid the 10% early-withdrawal penalty. The key is setting up payments to match your income needs while keeping as much flexibility in the rest of your portfolio as possible.

Benefits: allows penalty-free access to retirement funds before age 59½, avoids the need to take loans, can serve as useful bridge income during career transitions or early retirement, and helps you preserve non-retirement assets for other uses.

Main Items Covered:

Explain how 72(t) works

Walk through a practical example for a 56‑year‑old with an $800,000 IRA who requires just $15,000 per year

Outline the key pros and cons

Compare the 72(t) to the Rule of 55

Quick Overview: What is a 72(t) SEPP?

A 72(t) plan allows you to take penalty‑free withdrawals from an IRA before age 59½ if you agree to a schedule of “substantially equal periodic payments,” which must continue for the longer of:

5 full years or

Until you reach age 59½

Changing the schedule, altering the withdrawal amounts, taking extra distributions, or moving funds into or out of the SEPP IRA can jeopardize the arrangement and retroactively trigger the 10% early withdrawal penalty plus interest. Careful documentation and consistent, ongoing discipline are essential to preserve the plan’s tax benefits.

How payments are calculated (three IRS approved methods)

Required Minimum Distribution (RMD) method

Recalculates annually: Payment = prior 12/31 balance divided by the applicable life‑expectancy factor for that year.

Typically results in the lowest payment amount and fluctuates depending on market conditions.

Fixed Amortization Method

Level annual payment based on an allowed interest rate and life expectancy factor.

Current rules let you use whichever is higher: 5% or 120% of the mid-term AFR* (with an allowed look-back), so you can choose the higher rate.

Fixed Annuitization Method

Level annual payment calculated using an IRS-approved annuity factor

Usually quite similar to a fixed amortization schedule when evaluated using the same assumed interest rate.

You may make a one-time switch from a fixed method to the RMD method later (not vice-versa).

*Each month, the IRS provides various prescribed rates for federal income tax purposes. These rates, known as Applicable Federal Rates (AFRs), are regularly published as revenue rulings.

Example: A 56-year-old individual with an $800,000 IRA who requires approximately $15,000 per year.

If the entire IRA balance of $800,000 were applied in these calculations, the following results would apply: (based on current life expectancy tables, prevailing interest rates, and annuity factors in effect at the time of this Blog)

RMD method: $27,874 annual payout

Fixed Amortization: $53,085 annual payout

Fixed Annuitization: $54,237 annual payout

Because they only need $15,000 a year, transfer a portion of the IRA into a separate IRA (SEPP IRA) so it will generate the required annual payout.

Step 1 - Split into two IRAs

SEPP IRA: Holds only the amount needed to produce the $15,000 annual payment

Flex IRA (Original IRA): Holds the remaining assets to provide flexibility for Roth conversions, occasional or ad‑hoc withdrawals, strategic rebalancing, optimized asset location, and other opportunistic moves.

Step 2 - Size the SEPP IRA for $15,000 per year

Below are planning-level figures for a first-year start. Exact amounts will vary depending on the valuation date, the life expectancy or annuity factors applied, and the allowable interest rate selected at setup.

This income strategy should be used until the individual turns 59½ or for five years, whichever is longer, so the early‑withdrawal penalty ends. After that period, the individual could move any remaining SEPP IRA funds back into the original IRA and manage them together again if they desire.

Pros and cons of using 72(t)

Pros

Penalty-free access before 59 1/2

Precise income targeting by carving out only what you need

Predictable cash flow with the fixed methods

Cons

Locked in for at least 5 years (or until age 59½ if longer)

Risk of breaking the plan if you change the schedule or handle the SEPP IRA incorrectly (penalties apply)

Sequence risk when markets drop

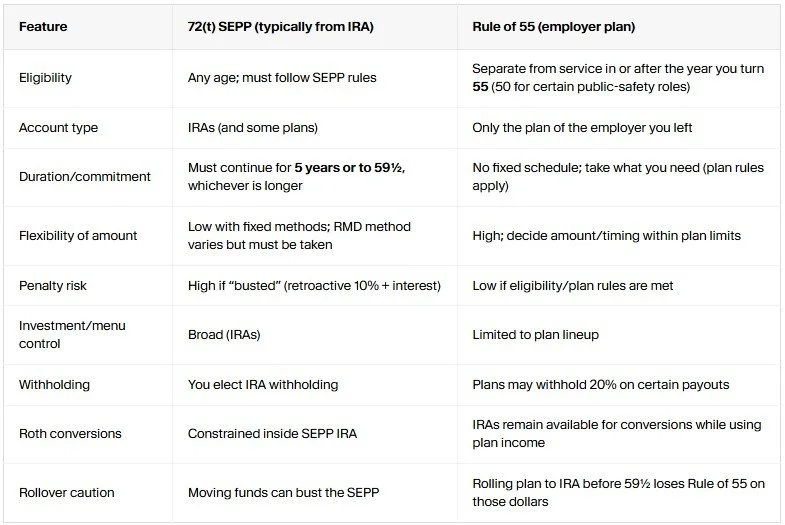

72(t) vs. Rule of 55 — Which option fits your situation better?

If your 401(k) or 403(b) plan allows penalty-free withdrawals under the Rule of 55 after you leave your job in or after the year you turn 55, that option is often simpler and more flexible than a 72(t) distribution. Here’s a brief comparison:

Additional Items for Consideration:

In the SEPP IRA, keep a 12–24 month cash or bond buffer.

Choose a payment schedule that matches your cash flow: monthly, quarterly, or yearly.

In the first year, you may take either the full annual amount or a pro-rata amount based on months remaining.

Keep the SEPP IRA untouched; use the Flex IRA for all other transactions.

Document everything: valuation date, chosen method, life expectancy factor, allowable interest rate and payment schedule

Coordinate tax withholding. If the custodian issues a 1099-R with Code 1 (early distribution), file Form 5329 and claim the 72(t) exception.

Reminder: you may make a one-time switch from a fixed method to the RMD method later (not vice-versa).

Need help setting up and documenting a 72(t) that fits your cash flow and taxes? Ville Wealth Management can design the carve‑out, build the portfolios, and manage everything so your plan stays on track.

Ville Wealth Management is a Registered Investment Adviser in the state of Ohio. Advisory services are only offered to clients or prospective clients where Ville Wealth Management and its representatives are properly registered or exempt from registration. “Likes” should not be considered a positive reflection of the investment advisory services offered by Ville Wealth Management. Brian Jaros is an investment adviser representative of Ville Wealth Management. The firm is a registered investment adviser and only conducts business in jurisdictions where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability. The information presented on this post is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Comments should not be construed as an offer to buy or sell, or a solicitation of an offer to buy or sell the investments mentioned. A professional adviser should be consulted before implementing any of the strategies discussed. Investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client's portfolio. All investment strategies can result in profit or loss.