Why Clients Are Coming to Ville Wealth Management

Taxes Shouldn’t Derail a Smart Transition

One of our recent clients came to us sitting on significant realized gains, nervous that moving to a better-suited portfolio would trigger a painful tax bill. Rather than forcing a wholesale change, we implemented a direct indexing strategy, giving them broad market exposure while maintaining individual security-level control. We set a quarterly capital gains budget and paired it with systematic tax loss harvesting, allowing us to transition thoughtfully over time without blowing up their tax situation. The result was a smarter portfolio and a much smaller tax headache.

Your Money Should Never Be Trapped

Several clients came to us frustrated and frankly surprised to discover that investments recommended by their previous advisor came with lock-up periods of five years or more. They had no idea until they wanted to make a change. At Ville Wealth, we operate with a simple principle: all assets are fully transferable and never locked in. Before we recommend any investment, we walk clients through exactly what they are getting into, including liquidity, risks, fees, and timelines. No surprises. No fine print you will regret later.

You May Be Paying Too Much

Fee transparency matters. Some of our newest clients were paying over 1.3% in annual advisory fees, year after year, without a clear sense of what they were getting for it. At Ville Wealth, our fee schedule is straightforward and competitive:

Ville Wealth Management Fee Schedule

Clients with portfolios over $3 million receive an additional discounted schedule. Over time, the difference in fees alone can compound into tens of thousands of dollars, money that stays in your pocket and continues to grow.

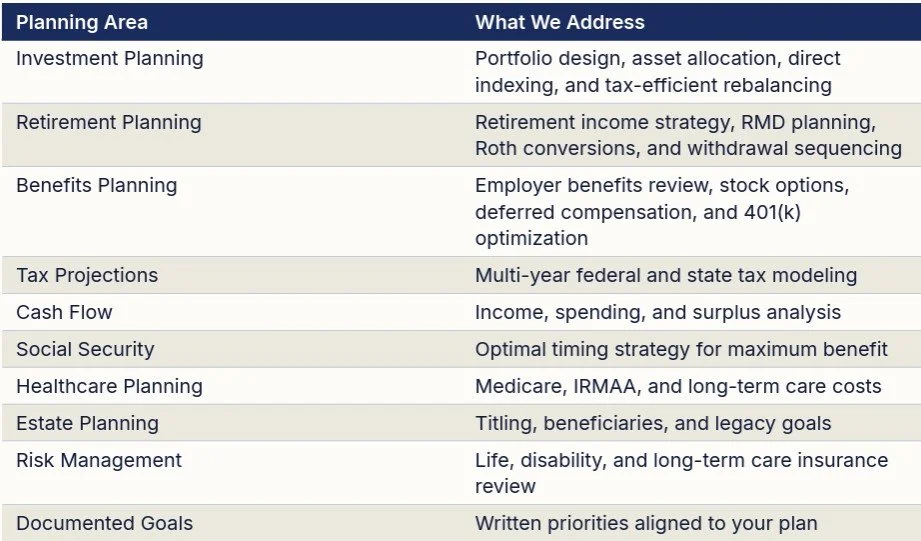

A Real Financial Plan Changes Everything

It might surprise you to know how many people have worked with a financial advisor for years, sometimes decades, and never received a comprehensive financial plan. We have met clients who had no documented goals, no tax projections, no cash flow analysis, and no strategy for Social Security timing, healthcare costs in retirement, estate planning, or insurance coverage. A portfolio alone is not a plan. At Ville Wealth, every client relationship begins with a thorough, forward-looking plan covering:

The Opportunity Valley: A Tax Problem You May Not See Coming

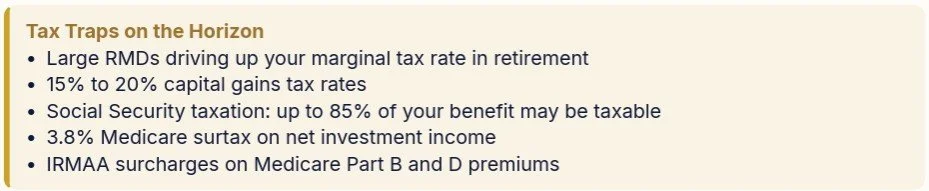

If you are over 50 and have successfully built substantial retirement accounts, congratulations. But be aware of a serious tax challenge ahead. For the past 30 years, federal tax rates have been historically low. However, with our national debt nearing record levels, higher future tax rates are a real possibility. And even if rates do not rise, when you turn 73 and Required Minimum Distributions (RMDs) kick in, your retirement accounts may be so large that those mandatory withdrawals push you into the highest tax brackets for the rest of your life. Large RMDs also trigger IRMAA surcharges, raising your Medicare Part B and D premiums to their highest levels.

The SECURE Act 2.0 made this even more urgent for families with wealth to pass on. Your heirs can no longer stretch distributions over their lifetimes. They must now withdraw all inherited retirement funds within 10 years. If your account is worth over $2 million when you pass, that could mean roughly $200,000 per year in forced withdrawals, likely pushing your heirs into the highest tax brackets as well.

The average retirement age in the U.S. is 65 for men and 63 for women. If you delay Social Security benefits to maximize them, which we often recommend, you enter a window of time with potentially much lower taxable income. That window is the Opportunity Valley, and it is one of the most powerful tax planning periods of your financial life. By strategically withdrawing from your retirement accounts during this window, you can take advantage of lower tax brackets, reduce future RMDs, and lower your overall lifetime tax burden.

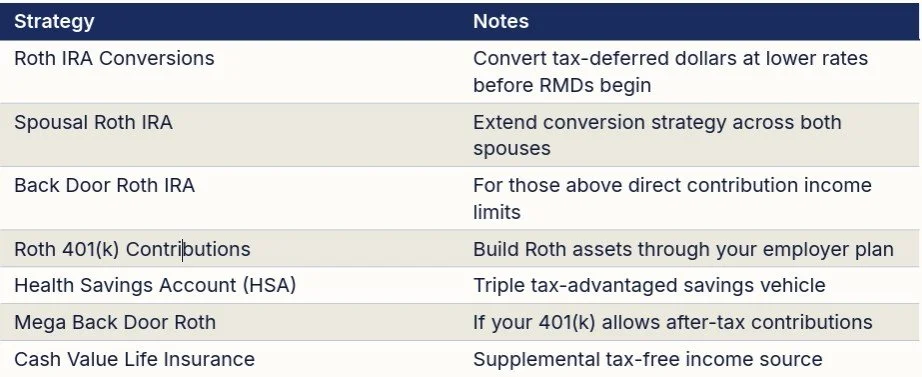

Strategies to consider for filling the Opportunity Valley:

A combination of Roth conversions with strategic retirement account withdrawals can help fill income gaps, reduce federal and state taxes, and keep Medicare premiums from skyrocketing. The Opportunity Valley is not a problem to fear. It is a window to act. Read more at villewealth.com/blog/opportunity-valley.

Performance Should Justify the Price Tag

Markets have been a proving ground lately, and some of our new clients arrived disappointed, not just by returns, but by what they were paying for them. Their previous managers were charging full advisory fees while relying on active management strategies that, over a 10-year horizon, the data consistently shows fail to outperform the market on average. In fact, only about 22% of active fund managers have outperformed their passive peers over the last decade. Paying a premium for underperformance is not a strategy. At Ville Wealth, we build evidence-based portfolios that prioritize low-cost, broadly diversified exposure, and we are transparent about exactly what you are paying and why.

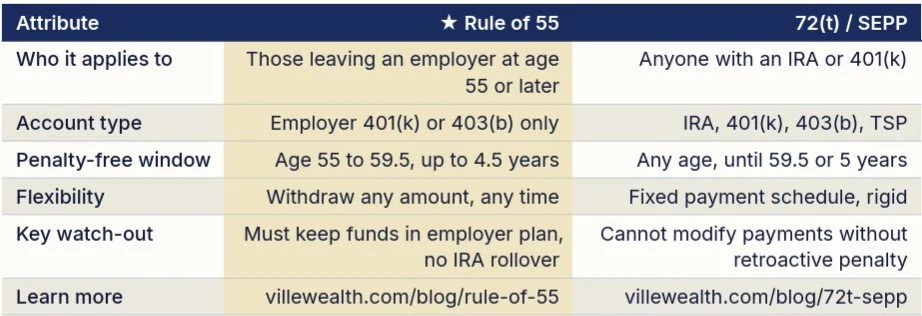

Under 59.5 and Need Access to Your Retirement Accounts?

One of the most common and costly misconceptions we encounter is that money in a 401(k) or IRA is completely off-limits until age 59.5 without paying a steep 10% early withdrawal penalty on top of ordinary income taxes. That is not always true, and it is a conversation that has changed the lives of several of our newer clients.

Two IRS-approved strategies can provide penalty-free access to retirement funds before age 59.5:

At Ville Wealth, we carefully evaluate whether either of these strategies fits a client’s broader financial picture, including income needs, tax bracket, long-term retirement outlook, and plan rules, before making any recommendation. If you are approaching 55, considering an early retirement, or simply need a bridge to your traditional retirement age, this conversation is worth having.

Ready to Have a Different Kind of Conversation?

If any of these stories sound familiar, we would love to connect. At Ville Wealth Management, you will get straightforward answers, a real financial plan, and an advisor who is truly in your corner.

Schedule a Complimentary Consultation Visit villewealth.com or call us today to get started. There is no cost and no obligation, just an honest conversation about where you are and where you want to be.

IMPORTANT DISCLOSURES

This material is for informational and educational purposes only and does not constitute tax, legal, or investment advice. Figures, strategies, and illustrations are provided as general examples and may not apply to your individual situation. Consult a qualified financial, tax, or legal professional before implementing any strategy discussed. Ville Wealth Management is a Registered Investment Adviser in the State of Ohio. Registration does not imply a certain level of skill or training. Past performance is no indication of future results.

Ville Wealth Management is a Registered Investment Adviser in the state of Ohio. Advisory services are only offered to clients or prospective clients where Ville Wealth Management and its representatives are properly registered or exempt from registration. “Likes” should not be considered a positive reflection of the investment advisory services offered by Ville Wealth Management. Brian Jaros is an investment adviser representative of Ville Wealth Management. The firm is a registered investment adviser and only conducts business in jurisdictions where it is properly registered, or is excluded or exempted from registration requirements. Registration as an investment adviser is not an endorsement of the firm by securities regulators and does not mean the adviser has achieved a specific level of skill or ability. The information presented on this post is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Comments should not be construed as an offer to buy or sell, or a solicitation of an offer to buy or sell the investments mentioned. A professional adviser should be consulted before implementing any of the strategies discussed. Investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client's portfolio. All investment strategies can result in profit or loss.